Introduction – The Transmutation of Risk

In thermodynamics, there is a law that states, “Energy is neither created nor destroyed, it can only be transformed from one form to another.” This first law rules the entire universe as an isolated system, when energy changes or is transferred, it is never destroyed, only transmuted. Over time, our financial system is becoming increasingly less volatile on an average day as outside forces attempt to subdue overall market volatility. At the core of the suppression of this every-day volatility lie increased competition, central banks, and computer algorithms which all continue to play their role in dialing down any given day’s expected fluctuation. Lurking behind this perceived tranquility is thermodynamics’ first law – “Volatility is never created or destroyed, only transmuted.” Displaced from the everyday fluctuations, this volatility must go somewhere. Volatility, like energy, cannot be destroyed, only transmuted. As the world reaches new frontiers of innovation and efficiency, the middle of the “bell curve” (if we can call it that) of daily market fluctuations grows thinner and thinner, suppressed by increasing numbers of market participants, artificial market interference, and algorithms, leaving volatility nowhere to go but into the tails of the curve. With greater interconnectivity and sophistication, positive feedback loops and black swans play a more active role in the world than in its prior years. We saw this in the flash crash of 1987, the housing crisis of 2008, and the volatility “apocalypse” of February 5, 2018. In this quarter’s investor letter, we’re taking the opportunity to dive deep on one particular aspect of Houndstooth Capital’s strategy. While we don’t normally devote this much attention to a single trade in the strategy, given the unprecedented nature of some of the volatility experienced in Q1 and its outsized influence on the fund’s returns, we thought it would be appropriate to spend some extra time going in-depth on what became the largest driver of returns for the quarter in addition to our normal market commentary. As the world modernizes and becomes increasingly interconnected, it is our belief that volatility will continue to migrate from the middle to the tails, which is exactly why we must be educated and prepared for such events as they play a more active role in our financial system.

Market Commentary

Mirroring the previous year, 2018 began with consistent, bullish price action. Backed by global growth, low inflation, historic tax cuts, and dovish monetary policy, the S&P 500 printed new all-time highs 14 of its 21 trading days in January – the most all-time highs in one month since June 1955. Following one of the most tranquil periods in market history, the S&P violently entered correction territory, suffering a 10.7% decline in just 6 trading days. February 5th delivered a 4.1% blow to the market on its own.

Volatility Overview

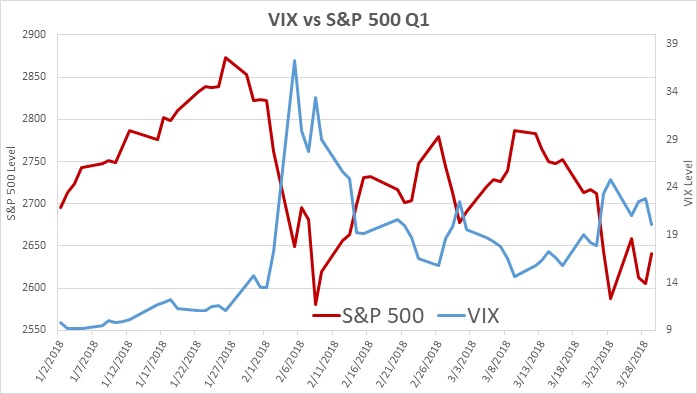

While equity markets’ moves were amazing to watch in Q1, the moves in the volatility markets were even more incredible. The following charts depict the S&P 500 vis-à-vis the VIX and the VIX futures throughout Q1 2018 respectively.

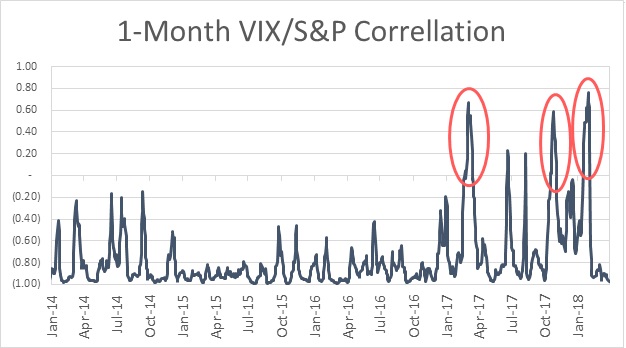

Prior to what some are now dubbing the “Volpacalypse” (Feb 5), the VIX was already behaving abnormally in January. It is rare to see the VIX consistently rise in concert with the S&P 500, but that is exactly what we saw in January. In our previous newsletter, we pointed out the bouts of weakening negative correlation between the S&P 500 and the VIX in 2017. The following chart continues the story of abnormal deviation of S&P and VIX correlation:

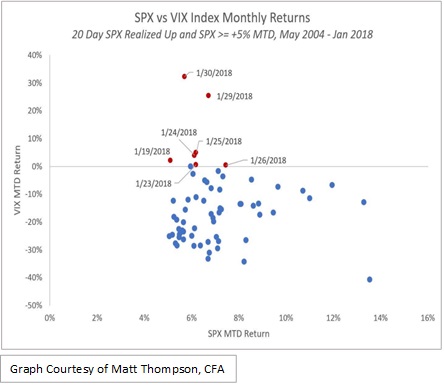

Furthermore, since 2004, never had a +5% month-to-date S&P gain been accompanied by a gain in the VIX. While the S&P continued to post new all-time-highs throughout January, the VIX also continued to climb. Demonstrating the consistency of this phenomenon, the following chart shows the corresponding VIX MTD returns for each day the S&P has shown a 5% MTD return since May 2004.

Did this anomalous positive correlation foreshadow the coming market turmoil? One could argue that the “smart money” did not have conviction in the historic rise in January and was buying protection all along the way. It could also be possible that sellers of covered calls were being forced to cover their calls as they continued to roll them up to higher strikes, thus bidding up options’ prices.

Did this anomalous positive correlation foreshadow the coming market turmoil? One could argue that the “smart money” did not have conviction in the historic rise in January and was buying protection all along the way. It could also be possible that sellers of covered calls were being forced to cover their calls as they continued to roll them up to higher strikes, thus bidding up options’ prices.

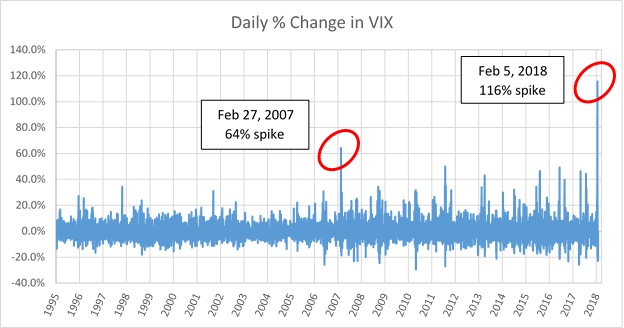

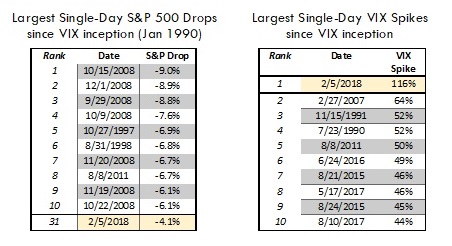

During the decline, the VIX spiked above 50 for the first time since the financial crisis. For the first time in history, the VIX experienced a daily gain over 100%, finishing February 5th up 116%. The previous largest single day spike was 64% in February 2007.

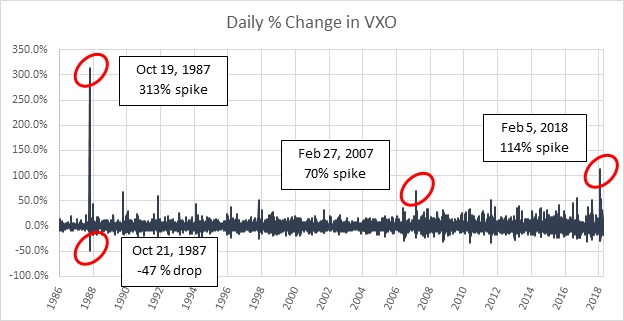

Since the data for the VIX in its current iteration only goes back to the early 90’s, it’s useful to examine the history of its sister index, VXO, when comparing February’s spike to the poster child of Black Swans – the flash crash of October 19, 1987. For background, VXO differs from VIX in that it is calculated using near-the-money S&P 100 options whereas the VIX uses a much broader range of available strikes on the S&P 500 Index. While the calculations differ, they do well in closely following one another. The below chart depicts the historical percentage changes in VXO since its inception, which includes Black Monday of 1987.

As previously mentioned, VXO demonstrates very high correlation to the VIX, as seen in February 2007 and February 2018. So, although VIX was not around on Black Monday, VXO’s representative spike of 313% dwarfs the 114% seen on February 5, 2018. From the 1987 spike in VXO, one could infer that a 100% daily spike in VIX (though never seen before in the VIX index itself) would certainly be a risk one could not predict but must protect against, specifically in the case of negatively levered VIX ETPs (more on this later). For purposes we will discuss later, it is important to note the -47% drop in VXO after its Black Monday rally. This risk presents an interesting predicament for positively levered VIX products. The opportunities of this overlooked phenomenon will be discussed in more detail later.

As previously mentioned, VXO demonstrates very high correlation to the VIX, as seen in February 2007 and February 2018. So, although VIX was not around on Black Monday, VXO’s representative spike of 313% dwarfs the 114% seen on February 5, 2018. From the 1987 spike in VXO, one could infer that a 100% daily spike in VIX (though never seen before in the VIX index itself) would certainly be a risk one could not predict but must protect against, specifically in the case of negatively levered VIX ETPs (more on this later). For purposes we will discuss later, it is important to note the -47% drop in VXO after its Black Monday rally. This risk presents an interesting predicament for positively levered VIX products. The opportunities of this overlooked phenomenon will be discussed in more detail later.

In regard to the VIX futures term structure, VIX traders remained surprisingly complacent after February 5th. For the longest duration in recent memory, VIX futures remained in backwardation for the majority of February and March. This is an interesting development, as it may be a sign of complacency as traders are not willing to bid up futures prices to keep pace with a higher VIX, but instead expect the VIX to revert to “normal,” lower levels. February saw a massive spike in realized market volatility. However, a volatility risk premium is still not priced in the market, despite the wild price action.

Anatomy of a Blowup

We thought investors would be interested in an analysis of exactly how Houndstooth came to hold its positions which benefitted so tremendously from the volatility spike on February 5th. To that end, we offer our interpretation of the unprecedented events in the volatility markets, why they occurred and how we came to hold an advantageous hedge.

Equity markets in the United States and even globally have seen historic gains in the almost 10 years following the Great Recession of 2008. During that time, stocks have climbed to record levels with some of the highest relative valuations ever seen. In that context, the losses witnessed by the S&P 500 over the course of a few days in February were rather pedestrian in the grand scheme of the market’s history. Although the market fell by 4.1% on February 5th alone, this one days drop ranks as the 31st biggest one day drop in the S&P since the VIX’s inception. While large, it paled in comparison to other massive shakeups in equities throughout history, especially those predating the VIX.

Equity markets in the United States and even globally have seen historic gains in the almost 10 years following the Great Recession of 2008. During that time, stocks have climbed to record levels with some of the highest relative valuations ever seen. In that context, the losses witnessed by the S&P 500 over the course of a few days in February were rather pedestrian in the grand scheme of the market’s history. Although the market fell by 4.1% on February 5th alone, this one days drop ranks as the 31st biggest one day drop in the S&P since the VIX’s inception. While large, it paled in comparison to other massive shakeups in equities throughout history, especially those predating the VIX.

However, for volatility markets, February 5th was orders of magnitude more impactful that just your run-of-the-mill drop in stocks. The VIX index witnessed its largest ever one day gain in history, roughly doubling the largest one-day spike dating back to 1990 when the VIX was created.

Comparing the largest drawdowns in the S&P 500 to the largest spikes in the VIX, it begs the question – what happened on February 5th that caused such a large disconnect between equities and volatility? Furthermore, was this really a disconnect at all and does it matter?

To unravel the answers to these questions, it’s important to first understand why it matters at all. The primary reason that spikes in the VIX are more meaningful today than ever before hinges on the nature of the trading ecosystem that has built up around volatility as an asset class. This ecosystem has the ability to reflexively impact equity prices and the broader economy as a whole.

For context, let’s first explore our interpretation of what exactly volatility is and how it is traded. At its highest level, volatility can be seen as the dispersion of movement of any unit of measurement across a discrete time period. Put more simply, it’s how much or little something moves. This can be applied to wind speeds, stocks, crop yields or the temperature on Mars. It stands then that by shorting volatility, one is making a bet that fluctuations in movement will stay below a certain threshold. A person with a short-volatility investment has traded risk in exchange for potential reward.

Consider that almost all investments of one kind or another are implicitly short volatility, usually without expressly intending to be. For example, a homeowner buys a house with an implicit short volatility bet against wind speeds even if that was not her intention when she bought the house. If wind speeds on average for a house’s given location averaged 15 MPH, with a standard deviation of 10 MPH, a homeowner would assume for example, that the house is likely to never blow over if wind gusts are normally distributed. However, wind speeds are not evenly distributed in the event of a tornado. In that scenario, although the house had never experienced a single wind speed above say 75 MPH, a tornado could bring in an instant, a single wind gust above 200 MPH, which could entirely wipe out the house.

Consider that almost all investments of one kind or another are implicitly short volatility, usually without expressly intending to be. For example, a homeowner buys a house with an implicit short volatility bet against wind speeds even if that was not her intention when she bought the house. If wind speeds on average for a house’s given location averaged 15 MPH, with a standard deviation of 10 MPH, a homeowner would assume for example, that the house is likely to never blow over if wind gusts are normally distributed. However, wind speeds are not evenly distributed in the event of a tornado. In that scenario, although the house had never experienced a single wind speed above say 75 MPH, a tornado could bring in an instant, a single wind gust above 200 MPH, which could entirely wipe out the house.

The same logic can be applied to investments in stocks, bonds, your own health, commodities, governments and myriad other domains in life.

Why does it matter? It matters because most investments have an implicit short volatility component, and this is natural. Companies, societies, families and portfolios are all constructed on the implicit premise that things will remain relatively calm. However, this is where the distinction between implicit and explicit volatility bets is important. To buy a house is to implicitly short the volatility of wind; buying home insurance is an explicit volatility bet on wind (as well as earthquakes, floods, fires etc.). Thought of a different way, explicit volatility trades are often “side bets” on the underlying asset.

These same principles extend to the United States equities markets. To understand the dynamics at play on February 5th, it’s important to appreciate the underlying bets and sides bets at work in the volatility ecosystem.

The Dog Wagging the Tail

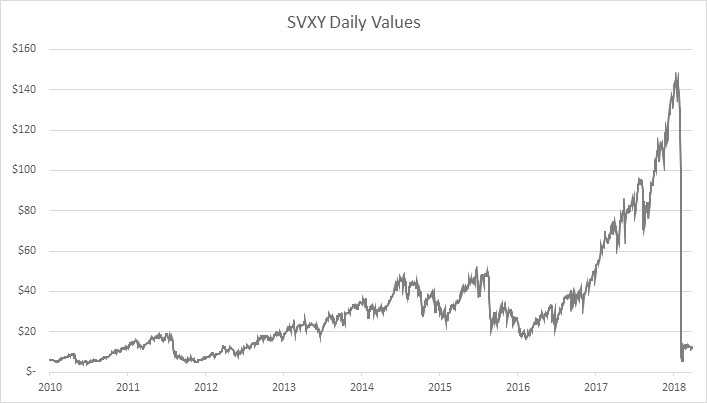

On February 5th, two Exchange Traded Products (ETPs) lost roughly 95% of their value in a single trading day, wiping out approximately $4.1 Billion of shareholder value in both products. Trade tickers XIV and SVXY were products issued by Credit Suisse and ProShares respectively and were designed to track the performance of a rolling 1-month duration VIX futures contract portfolio with a leverage factor of -1X. In the landscape of volatility instruments, these traded near the tip of the “dog’s tail.” The chart below shows the price of XIV for the last 5 years of trading, ending with its abrupt collapse on February 5th.

Both XIV and SVXY had become increasingly popular among retail traders as a means of trading volatility. However, the functional structure of both products caught many market participants off guard when in a matter of only a few hours, they became almost worthless. How and why these products behaved the way they did is crucial to understanding the landscape for volatility trading going forward.

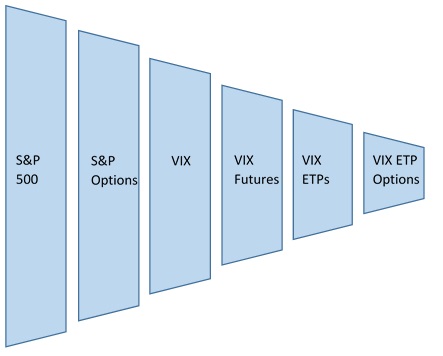

The chain of volatility-related products is complex, but crucial for understanding the mechanics behind the meltdown. The S&P 500 is composed of component stocks that, in aggregate, derive the S&P 500 Index value. Options are traded on the index going out anywhere from days to years. A basket of options with an average expiration of 30 days is used to impute the VIX index. Simply put, the VIX is a single measurement of how costly options on the S&P 500 are in the near future. It’s crucial to note, that the VIX itself is not tradable since it is only a measurement. The VIX is like taking the temperature outside. Bets can be placed on where the temperature may land on a given day, but the temperature itself cannot be bought or sold. VIX futures are contracts that expire monthly based on the level of the VIX at expiration. These futures are the equivalent of bets on what the temperature will be at a particular date and time.

The VIX futures trade with contracts going out up to 8 months into the future. Various VIX ETPs trade around numerous strategies related to holding VIX futures. There are several ETPs with varying leverage, mechanics and durations, but the most popular products (as measured by Asset Under Management) focus around a portfolio of either long or short rolling 1-month VIX futures. Finally, some but not all the of the VIX ETPs have options traded around them. For instance, XIV and SVXY were structured to produce almost identical returns, however XIV did not have available options traded on it, while SVXY did. After stepping back, the chain is revealed from the S&P to S&P options to the VIX to VIX futures to VIX ETPs to VIX ETP Options – side bets on side bets on side bets. The entire ecosystem is mechanically linked, creating opportunities for dislocation and arbitrage throughout.

Mechanics of Levered and Inverse ETPs

Volatility is by no means the first or only asset class with ETPs seeking to deliver levered and/or inverse daily returns for an underlying asset. A whole ecosystem of ETPs has become increasingly popular, delivering between -3X and 3X the daily returns for assets ranging from the S&P 500 to gold and even currencies. ProShares alone has over 100 levered and/or inverse ETPs available to retail investors. Inverse and levered ETPs use leverage and derivatives to replicate the daily return of their underlying index or asset.

Crucially, these products must rebalance daily in order to maintain their target exposure to the underlying product or index. This is critically important because it has two profound impacts which were instrumental in the blow up of XIV and SVXY.

- First, by resetting leverage daily, these products must trade at the end of the day in order to rebalance. This end of day rebalancing can create a flood of volume driven by the products’ need to rebalance all within a short time period.

- Second, because these products trade with set leverage amounts, the amount of trading that must be undertaken on behalf of these products is known and quantifiable on a daily basis.

Typically, the daily rebalancing of levered and inverse ETPs can go unnoticed. Assuming first that the products themselves don’t represent a disproportionate share of the outstanding interest in the underlying instruments and, second, that the underlying instruments don’t move too much, rebalancing can occur seamlessly. You can guess what went wrong in the case of XIV and SVXY.

One more important aspect of levered and inverse ETPs is that by resetting daily, they are disproportionately affected by large drawdowns as realized volatility increases. For example, a -1X levered fund that experiences a 10% decline in a single day (for example from $100 to $90) would need a subsequent gain of 11.11% to breakeven. The disproportion between a given drawdown and the subsequent gain required to bounce back increases exponentially as returns approach -100%.

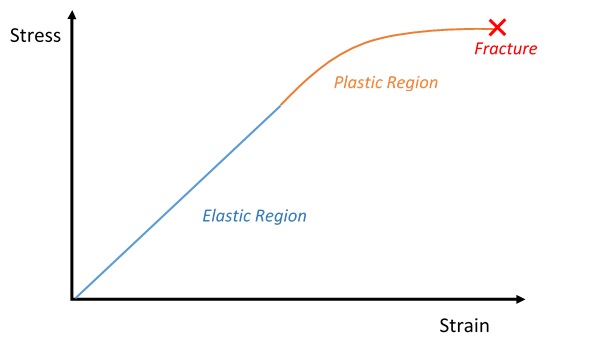

In materials science, there is a similar destructive property of solids called plasticity. When a small force is applied to a solid, many solids will be elastic, meaning they will compress as force is applied. But once the force is no longer applied, the solid can reassume its former shape naturally. However, most solids have a point of plasticity whereby as more force is applied, the solid will permanently deform, unable to regain its former shape naturally. Eventually, given enough force, the solid will fracture entirely.

Just like in materials science, -1X levered ETPs have a sort of plasticity whereby it becomes almost impossible to regain lost ground, given a loss of significant magnitude. While it isn’t an exact science and data are limited, even a short trading history of XIV maps drawdowns in the product with the time period and magnitude required to recoup losses, mapping a rough estimation of XIV’s “plasticity.”

Just like in materials science, -1X levered ETPs have a sort of plasticity whereby it becomes almost impossible to regain lost ground, given a loss of significant magnitude. While it isn’t an exact science and data are limited, even a short trading history of XIV maps drawdowns in the product with the time period and magnitude required to recoup losses, mapping a rough estimation of XIV’s “plasticity.”

Not only is this academically interesting, but for practical purposes, the built-in mathematical plasticity of these products made them the best candidate for a tail-event hedge. An alternative method of hedging a spike in volatility would be to buy call options or futures on the VIX directly. However, VIX futures and VIX options holders had to get the timing perfect to capitalize on their fleeting opportunity, since these derivatives quickly reverted back to lower levels after the VIX spike. Unlike direct hedges through the VIX, those who found efficient ways to short the VIX ETPs did not have to worry about timing; the large sum of their profits was mathematically locked in by the plastic nature of SVXY and XIV once volatility spiked.

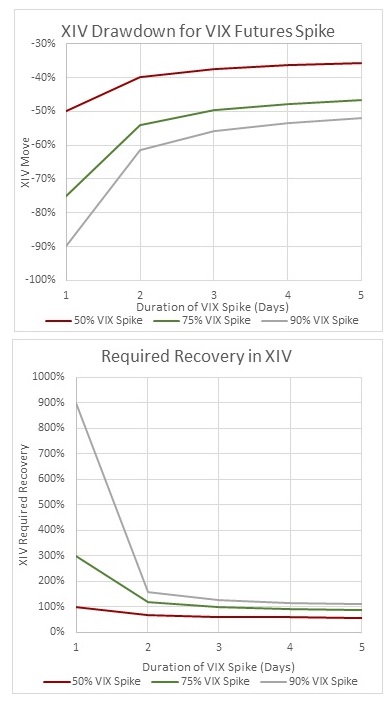

One final note on the nature of drawdowns and recovery for levered ETPs: they are highly path dependent, unlike normal securities. What this means is that the path that the underlying asset or index takes matters. In this particular case, it was not just the magnitude of the VIX spike but more importantly the velocity of the spike that spelled doom for the negatively levered funds.

For these products, the faster the VIX futures spike, the greater the damage dealt to XIV and SVXY. The chart to the right illustrates the drawdowns XIV would have experienced given spikes in VIX futures of varying degrees, lasting from 1 to 5 days. For the spike of equal magnitude, taking one day to reach its destination is far more damaging to XIV than if the VIX futures were to take the same trip spread over multiple days.

For example, a 90% spike in VIX futures would cause XIV to decline by 90% if the spike occurred in a single day, leaving XIV with a 900% required recovery to bounce back. The same 90% spike in VIX futures spread equally over 5 days would only result in a drawdown for XIV of 52%. In that scenario, XIV only needs a 108% gain to recoup its losses. The graph to the right illustrates these consequences for the same scenarios described in the previous figure.

Rebalancing

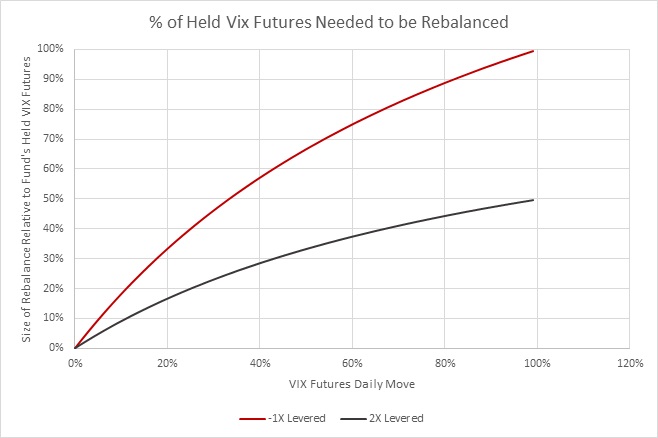

The final piece to the XIV and SVXY implosion puzzle is the mechanical rebalancing process all levered ETPs must abide by to maintain target leverage. For -1X levered products, as their underlying asset or index rises, the amount of the asset these funds have to trade to maintain leverage rises proportionately. As the underlying asset rises, the -1X ETP must buy back shares of its tracked asset to cover its short position. Conversely, if the underlying were to fall, the -1X ETP would need to sell some of its position to maintain the proper leverage.

-1X & 2X Levered ETPs Buy and Sell Shares TOGETHER

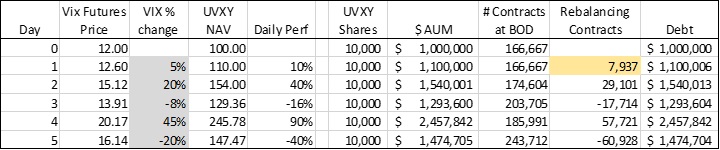

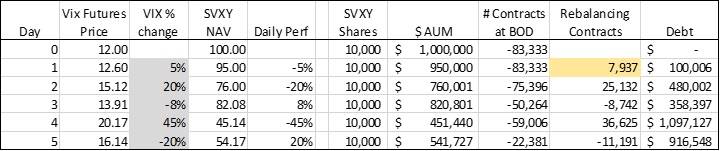

Perhaps one of the most counter-intuitive aspects of levered ETPs tracking the same underlying index or asset is that -1X and 2X levered ETPs put the same buying pressure per dollar of Assets Under Management (AUM) on the underlying to rebalance, rather than offsetting positions. Essentially, after a rise in the underlying, -1X ETPs must buy back shares to cover a short position. At the same time, 2X ETPs must buy the exact same number of shares (given equal AUM of the two ETPs) in order to maintain enough leverage to generate a return twice that of the underlying.

The table below demonstrates this phenomenon for hypothetical 2X and -1X levered ETPs.

2X UVXY Required Rebalancing Scenario

-1X SVXY Required Rebalancing Scenario

Now that we’ve discussed the volatility landscape and levered ETPs, the stage is set for the blowup of XIV and SVXY. Remember these products are required to rebalance at the end of every day by either buying or selling VIX futures. The exact amount of futures required for rebalancing among the various VIX levered ETPs is known in the market. It is a simple function of the daily change in the VIX futures and the outstanding size of the ETPs.

At its heart, the blow up of XIV and SVXY all came down to a massive liquidity squeeze in VIX futures.

Tail Wagging the Dog

The relative size of derivatives or “side bets” to the underlying asset or index matters immensely. Why? Because price changes in the side bets can become reflexive on the underlying.

Imagine there are limited rules surrounding betting on boxing matches. Now imagine a prize fight in which the winner of the fight was to receive a cash prize of $10 million. Say there are side bets on the outcome of the fight worth $500 million in total. One can now easily imagine the scenario in which a gambler would be better off by paying one of the fighters $20 million to throw the fight and make up the difference from his side bets.

Alternately, an investor who was able to amass a huge number of puts on a company, could theoretically reach a point at which the side bets on the company were more valuable to her than the company itself. At that point, the investor could buy up the company in order to intentionally bankrupt it and collect on her side bets (assuming this was legal).

Why does this matter to VIX ETPs? Because the relative size of the ETPs to the size of the VIX futures market had become massive. When VIX ETPs initially were sold to the retail market (starting in 2009), most of the interest was in long volatility exposure products such as VXX (1X) and UVXY (2X Leverage). These products provided retail investors with a crude vehicle to benefit from spikes in volatility. However, these products have flaws of their own which over time massively eroded the value of these vehicles. While not great products, these long volatility ETPs mostly succeeded in providing some form of a hedge against an equity portfolio.

Fast forward through time and the S&P 500 has witnessed historically low levels of realized volatility since 2009. The underlying cause of such low levels of volatility is debatable and a discussion for another time. However, one of the emerging heroes of the low volatility levels was the consistently strong performance of -1X levered VIX futures ETPs (XIV and SVXY). Like any good investment that performs well consistently, these ETPs attracted capital – lots of capital.

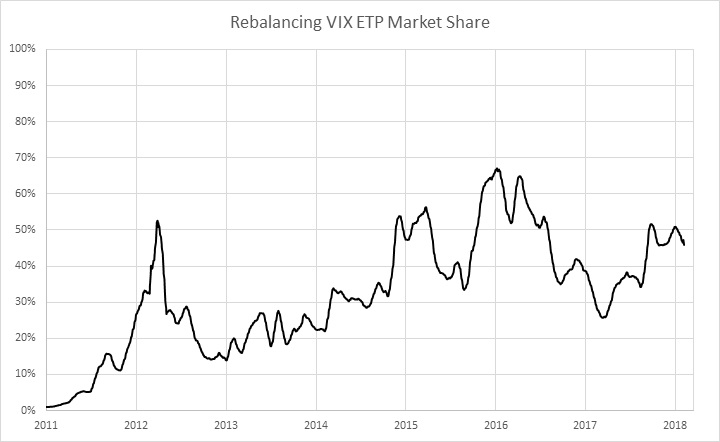

At the same time, the market for VIX futures themselves continued to grow. The absolute size of VIX ETPs is important, but more important is their relative size compared to the actual VIX futures themselves. As long as the ETPs make up a small share of the outstanding interest in VIX futures, rebalancing of the ETPs daily can easily be absorbed in the market. However, this did not remain the case. The chart below shows the size of -1X and 2X VIX futures ETPs relative to the size of the VIX futures open interest. Remember it’s important to look at both the -1X and 2X levered ETPs together since they create the same daily buying and selling pressures on VIX futures through rebalancing.

What Went Wrong

Given the above context for exactly how XIV and SVXY work in the context of volatility trading, it’s easy to see where this is heading. On February 5th, 2018 the S&P 500 fell by 4.1%. As mentioned previously, in the long context of history, this was a moderate, albeit painful pullback for the market. More surprising for the market was the magnitude of the move in the context of realized market volatility for the past year. In 2017, the S&P 500 did not experience a pullback of any duration of more than 2.8%. That mark was quickly eclipsed on February 5th.

Given the large drop in the S&P 500, its very reasonable to expect a spike in the VIX. The exact amount of the VIX spike both in percentage change terms as well as absolute level depends on many factors and can never be precisely estimated. The relationship of the VIX to the S&P 500 is a limitless topic for discussion which we won’t dive into here. Suffice it to say, that the 116% spike in the VIX on February 5th was disproportionately large relative to the move in equities. However, the outsized move in the VIX alone was not what brought death to the short volatility ETPs.

By 4pm on February 5th, with the VIX up roughly 90%, the near month VIX futures had risen by around 34%. This percentage change alone would have severely damaged the -1X VIX ETPs, however, the drawdown would have been far from sufficient to wipe them out completely. That damage came in the 15 minutes from 4 to 4:15pm.

Given the outstanding size of the combined -1X and 2X levered VIX ETPs and the 34% rise in near month VIX futures, these ETPs collectively needed to buy approximately 275,000 VIX futures contracts at 4pm to maintain their daily leverage functions.

For context, the 275,000 VIX futures that these ETPs needed to buy represented roughly 20% of the total outstanding interest in VIX futures and roughly 49% of the average traded volume of VIX futures for the previous 5 days. This was a massive amount of liquidity for the market to absorb, let alone in the span of 15 minutes at the end of a large down day for the stock market. As the buying of these contracts bid up the prices, even more contracts were needed for rebalance, thus accelerating the spike even further up by 4:15, as seen on the chart below. The chart below illustrates the volume of VIX futures traded to rebalance -1X and 2X VIX futures ETPs relative to the total open interest in VIX futures.

To reiterate, 1 of every 5 near term VIX futures contracts in existence needed to be bought in 15 minutes.

Looking back at the price elasticity of VIX futures trading at the end of days in which VIX futures spiked is an inexact sciene at best given the limited data set. However, suffice it to say that almost any market given the same trading volumes and time constraints to trade a record volume in 15 minutes would be expected to experience similar shocks to prices.

In short, the market makers that provided liquidity to VIX ETPs required to rebalance squeezed prices higher and higher. This created a devastating feedback loop for the ETPs. As prices for VIX futures spiraled higher, so did the required number of shares for rebalancing. Essentially these ETPs were forced to chase the prices of VIX futures higher and higher until they crossed their point of elasticity, irreparably breaking the products indefinitely. As an aside, short interest in VXX and products like UVXY was surely challenged by margin calls during this event. These no doubt added to the cascading buying of VIX futures, though its effect is less quantifiable.

Who Could Have Seen This Coming?

In short, no one. And also, anyone. The preceding post mortem of these products may make their demise seem obvious, but it was anything but a foregone conclusion, especially in regard to the timing of the collapse. Anyone claiming to have “predicted” the dramatic collapse of XIV and SVXY prior to February 5th is likely either lying or has a loose definition of prediction. Also, a prediction without a time horizon is not really a prediction. For example, we predict a volcano will erupt in North America at some point in the future causing massive devastation.

Despite the idiosyncrasies and structural flaws in these ETPs outline above, it was by no means a foregone conclusion that these produces had to or would blow up in the way they did, and certainly the timing could not have been predicted. There were of course warning signs such as the relative size of the products which made their collapse more probable, but ultimately unpredictable. XIV and SVXY could have carried on as they had for years without witnessing the kind destruction in value that they did.

However, despite any of the preceding analysis of these products, anyone who took 15 minutes to read the prospectuses of XIV and SVXY would have read the direct and clear warning statement: “The long term expected value of your ETN is zero. If you hold your ETN as a long term investment, it is likely that you will lose all or a substantial portion of your investment.”

Of course, this may seem like the Monday morning quarterback effect of realizing that buried beneath a mountain of other warnings and legalese in these prospectuses were myriad of warnings designed to indemnify the underwriters from liability in the event that anything were to go wrong.

In the aftermath of the collapse of XIV and SVXY, we received requests for commentary from journalists interested in our positions that paid out as these products collapsed. Of particular interest was how we were able to correctly predict the collapse of these instruments. We didn’t. Why then did we bother to hold positions that paid out massively in the event of the collapse in these instruments and why in the size that we did? The short answer is convexity, asymmetric payoffs, hedging and the mispricing of tail risk.

Think back to our example of the home owner who buys a house only to have it blow away in a tornado. The homeowner bought insurance on the house, but why? Did he correctly predict that a tornado would hit his house? Of course not. A tornado was only one calamity out of many that could have befallen his house. Although the homeowner was likely aware if he lived in an area prone to tornados. Depending on the specifics of his policy, the homeowner would have been protected against storms, floods, fires, earthquakes, tsunamis, terrorists, etc.

Buying a house without insurance is more profitable than buying a house with insurance right up until the point that the house is destroyed. However, just going out and buying lots of insurance on houses that you don’t own and hoping for disaster to strike as a means of investing is not a winning recipe either. Similarly, if you bought a house 20 years ago for $200,000, you would be foolish to insure it for that same amount today if the market value of the home had tripled in that time frame. That’s because you have no idea when calamity may strike your house, only that it is possible.

Similarly, we protected our portfolio against spikes in volatility in part through deep out of the money puts on SVXY. However, this is not because our entire portfolio consisted exclusively of a long SVXY position, but rather, these puts represented the most cost-effective hedge with the most asymmetric payoffs in our favor in several scenarios.

Even more importantly, this specific hedge allowed us to hedge against a volatility spike without requiring perfect timing on the exit, due to the previously discussed plastic nature of the product. This was also not our only form of protection for the portfolio, but certainly the most relevant for the purposes of this letter. It was also the most mispriced and effective.

We identified the massive liquidity squeeze which befell the -1X levered ETPs as one of many possible scenarios which could have destroyed these products. However, this was not nearly the only way they could have gone bust. For example, recall that the structural properties of these ETPs subjected them to path dependence and what’s called beta slippage. Essentially, these same products could have easily been eroded by a large increase in the realized volatility of volatility. Alternately, a prolonged period of backwardation in the VIX futures term structure could have also severely eroded their value as could have several other scenarios arising from increased volatility.

Anatomy of a Blowup – Epilogue

In the wake of the February 5th event, VIX futures remain in backwardation as traders seem to be continuing to wait for the VIX to return to mid-teen levels after it consistently hovered in the 20’s for the second half of Q1. One might expect the VIX futures to adjust for higher VIX levels, but they remained complacent for the second half of Q1. Currently, traders of VIX futures are selling implied volatility at a discount to realized volatility in Q1, which has historically been a dangerous strategy.

February 5th left in its wake a massive public relations nightmare for ProShares and Credit Suisse who were both accused of “irresponsibly” issuing these negatively levered products to uneducated, unsophisticated retail traders who didn’t fully appreciate the risks of holding these products. As a result, Credit Suisse announced that they would dissolve XIV which now no longer trades. However Proshares took a different approach to combat the PR nightmare. As the issuer of SVXY and UVXY, Proshares unexpectedly slashed the leverage of its two products from -1X and 2X to -0.5X and 1.5X respectively. The change was announced and implemented in a rushed 24 hours. This short-sighted and reckless move was likely designed to quell negative publicity in an attempt tone down the “danger” of these products by simply reducing the exposure of both ETFs to VIX futures. It could have also been a forced change as ProShares’ broker adjusted margin requirements and effectively limited the amount of exposure it would allow for the two products. However, while the SVXY and UVXY prospectuses warn that the ETFs may not fully achieve their target leverage due to broker requirements, it does not allow for an outright change in target exposure. Furthermore, the press release from Proshares announcing the change did not mention broker pressures as a cause for the adjustment. This seems like blaming their broker would have been an easy scapegoat for ProShares and potentially shielded them from liability in a class action lawsuit. In addition, Credit Suisse still maintains a 2X levered ETP (TVIX) which is not being adjusted, suggesting that at least Credit Suisse’s broker will continue to support the leverage required for the twin product to UVXY.

Certainly, reducing target leverage seems to only kick the can to a later date where we see another “never before” event, only greater in magnitude. For example, it’s easy to imagine even greater amounts of capital flocking into the adjusted -0.5X SVXY if it becomes perceived as “safer”, putting even greater rebalancing pressures under extreme events. However, even this instrument is destined to blow up upon the next “black swan” event that spikes VIX futures by record amounts. It’s certainly very plausible that a Black Monday type event would be enough to do the job.

Even more sinister, however, are the implications of what this myopic move by ProShares did to the holders of these products, the holders of their derivatives and anyone investing in levered ETPs in general. When Proshares abruptly modified the horsepower (leverage) of these products, it unilaterally and immediately created winners and losers in the options market for SVXY and UVXY. If SVXY is only half as powerful as it was just two days before, the option’s prices are now worth half or less than half of what they were once worth. This is like taking bets that a rocket can make it from New York to California in 2 hours, then once bets are in, announcing that the rocket is now a Vespa. Good luck getting to California on time now. While some publications covered this event as an atypical loss for just for options traders, this scandal was far more pernicious than what the public was led to believe. The responsible thing to do for Proshares would have been to create completely different products with different leverage levels and then market them to investors.

But why, after all, would Proshares do the appropriate thing when it could maintain its AUM in SVXY and avoid the cost of marketing a new product? Even better for ProShares, by adjusting the leverage of SVXY and keeping the product intact, they were able to gain the market share abandoned by Credit Suisse’s XIV, which was closed down.

Overlooked in the aftermath of ProShares decision to change the leverage of SVXY are the implications for investors in all inverse and levered ETPs. The SVXY prospectus stated nowhere that ProShares had the authority to unilaterally adjust the target leverage of the product. This precedent sets the stage for ETP issuers to dramatically change the very nature of products which have been sold to investors. In this case, ProShares wanted to avoid some bad PR, however, this precedent would allow an issuer to change an ETP’s target exposure to the massive enrichment of the issuer. Worse still are the implications for the Chicago Board of Options exchange which seems to be allowing this change without intervention. Its stands to reason that the options markets for these ETPs should massively reconsider the risks associate with holding options now that it has been established that the issuers can within a matter of hours change the risk profile of the products with no warning, or regard for consequences and all without disclosing these risks in the prospectus filed with the SEC. ProShares wiped out an estimated $100 million in value for options holders on SVXY and UVXY alone, but the precedent has the ability to destroy much more value in the future. While we aren’t legal experts, it seems that ProShares may be opening themselves up to substantial liability and should in our opinion face regulatory scrutiny for this decision. It should be noted that Houndstooth Capital Partners was not directly harmed by this change, as we did not hold options on these products at the time of the announced change.

Value for the Future

Going forward, what can we take out of this? First, this is a prime example of trying to fit a normal distribution to fat-tailed distributions on the VIX and VIX related products. Tail risk has been repeatedly shown to be often both systematically underestimated in frequency and devastating in effect. Second, this event and the findings from it lead to interesting implications for all other levered ETFs and their options. Finally, with the collapse of XIV and SVXY at the top of mind for many volatility traders, we suspect that other hidden risks are not being fully appreciated in long levered volatility ETPs such as TVIX and UVXY. While the funds reliably lose 90% of their value almost every year, we believe they also have blowup risks and the ability to collapse in similar fashion as SVXY and XIV. As mentioned in the introduction, VXO spiked over 300% on Black Monday of 1987. This would have no doubt been a great day for 2X levered UVXY holders had the product been in existence at the time. However, a harrowing day would soon follow when the VXO then fell by 47% in one day. This volatility exhale could have easily wiped out UVXY assuming the VIX futures would have similarly declined by around 50%. It’s easy to imagine a fleeting wave of panic spiking the VIX by a huge amount only to reverse course quickly. Imagine for example a false alarm of a nuclear warhead at the end of a trading day. Or imagine an unpredictable politician announcing major economic policies detrimental to growth only to soften his plans in short order. Such a spike and subsequent flash crash in the VIX could easily wipe out all previous gains for long volatility holders and then some.

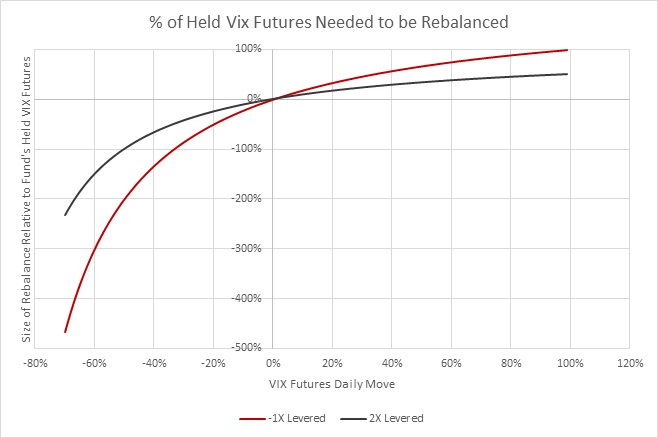

Importantly, it should be noted that the same rebalancing effect that worked against SVXY and XIV this time, would work against products like UVXY in a reverse scenario. In fact, it would be exponentially worse should the VIX have a substantial percentage loss in one day. The following chart shows the rebalancing required in the case of a VIX spike.

This is what sunk the inverse ETP’s – all of the funds, 2X and -1X, had to rebalance in the same direction. What others aren’t noting is how this rebalancing curve continues on the opposite side of the x and y axes. In the case of a VIX spike, the rate of increase in the number of contracts needed to rebalance tapers off with greater magnitudes of VIX gains. However, in the case of a VIX crush (VIX decrease), the number of contracts required for rebalance increases exponentially with percentage change in VIX futures.

As seen in the chart above, the magnitude of the required rebalance from a VIX spike like the one of February is quickly dwarfed by the required rebalance in the scenario of a black-swan VIX crush. Instead of being forced to buy to rebalance, violently bidding VIX futures prices up, these funds would be forced to sell to rebalance, dragging VIX futures prices precipitously down. One could only imagine the scenario where the VIX ETPs had a similar disproportionate size to their underlying asset’s open interest on a day like the -47% VXO crush two days after Black Monday of 1987. This is just one such specific risk that we believe the market is mispricing as it pertains to volatility instruments going forward.

HCP Update

While the positive VIX-S&P correlation in January was a drag to many in the short volatility complex, its pain was quickly eclipsed by the February 5th collapse of the VIX ETPs. The first quarter of the year was certainly one for the history books. Despite these challenging environments, Houndstooth managed to deliver a strong return for Q1 thanks to its choices in risk management measures. For a long time, we’ve maintained an outsized supply of deep OTM puts on SVXY to hedge our short volatility positions in case of an unforeseen black swan event. Though it has up until now been a drag on the fund’s performance, the unprecedented events in February led to these positions not only protecting the portfolio but also delivering positive returns. Covering this trade and the aftermath surrounding it, Houndstooth received coverage from publications including the Austin Business Journal, Quartz, and Reuters.

In February, we preemptively alerted our investors that the portfolio remained strong because in the wake of February 5th, many short-volatility funds made headlines losing anywhere from millions to billions of investor dollars. Interestingly, even tail-risk funds underperformed versus what one might expect they would deliver during such an event. Historically, tail risk funds have experienced gradual losses through the years with some funds delivering 8-20% losses last year, with the promise to outperform during market turbulence. These same funds only managed to deliver on average between 0-2% gains from February, according to a recent Wall Street Journal article. This was largely due to rapid reversals in equities and volatility which made timing profitable exits of hedges difficult. Highlighting the losses in February for many on both sides of the volatility trade, this Wall Street Journal article can be found here.

As previously mentioned, a modernized and interconnected world comes with its own victories and vices. While transmutation of risk continues to squeeze volatility from the middle of the curve into the tails, black swans will grow in frequency and impact. However, we must find creative ways to prepare for this or otherwise risk blowing up or bleeding slowly, waiting for the worst to occur. Regardless of how it is expressed, protection from tail events like the event of February 5th will only increase in importance as our world grows more sophisticated, interconnected, and driven by derivatives.

DISCLAIMER

THIS IS NOT AN OFFERING OR THE SOLICITATION OF AN OFFER TO PURCHASE AN INTEREST IN HOUNDSTOOTH CAPITAL PARTNERS, LP (THE “FUND”). ANY SUCH OFFER OR SOLICITATION WILL ONLY BE MADE TO QUALIFIED INVESTORS BY MEANS OF A CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM AND ONLY IN THOSE JURISDICTIONS WHERE PERMITTED BY LAW.

AN INVESTMENT IN THE FUND IS SPECULATIVE AND INVOLVES A HIGH DEGREE OF RISK. OPPORTUNITIES FOR WITHDRAWAL, REDEMPTION AND TRANSFERABILITY OF INTERESTS ARE RESTRICTED, SO INVESTORS MAY NOT HAVE ACCESS TO CAPITAL WHEN IT IS NEEDED. THERE IS NO SECONDARY MARKET FOR THE INTERESTS AND NONE IS EXPECTED TO DEVELOP.

THE FEES AND EXPENSES CHARGED IN CONNECTION WITH THIS INVESTMENT MAY BE HIGHER THAN THE FEES AND EXPENSES OF OTHER INVESTMENT ALTERNATIVES AND MAY OFFSET PROFITS. NO ASSURANCE CAN BE GIVEN THAT THE INVESTMENT OBJECTIVE WILL BE ACHIEVED OR THAT AN INVESTOR WILL RECEIVE A RETURN OF ALL OR PART OF HIS OR HER INVESTMENT. INVESTMENT RESULTS MAY VARY SUBSTANTIALLY OVER ANY GIVEN TIME PERIOD.